In December 2025, ClimeFi ran a request for proposals (RFP) for durable carbon dioxide removal (CDR) on behalf of a client expanding their portfolio. Submissions were received from 142 projects, representing 114 suppliers across 39 countries, covering multiple CDR pathways.

In our latest ClimeFi insights article, we provide an overview of the market dynamics that we have observed emerging from the recent RFP dataset. For a full breakdown of how we conducted the analysis, please refer to the ‘Behind the analysis’ section at the end of the article.

Tightening supply, converging prices

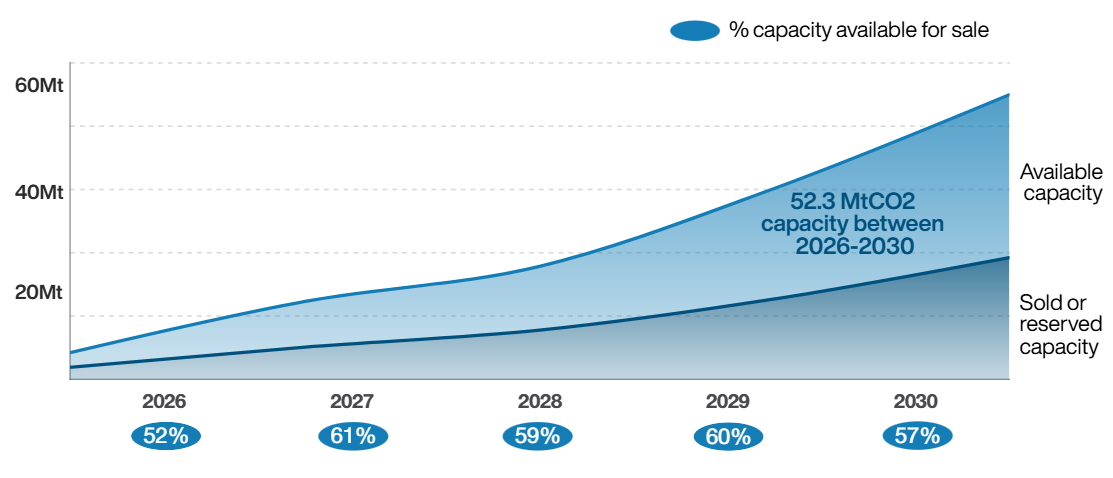

Despite projected capacity scaling significantly through 2030, just 58% of that supply remains unreserved across the 2026-2030 period, with 2026 the most constrained at 52%.

Though reserved capacity may include supplier-withheld volumes and operational buffers, availability remains just over half across every vintage, suggesting that buyers are actively securing volumes beyond just the near term.

Figure 1: Cumulative CDR capacity (MtCO₂)

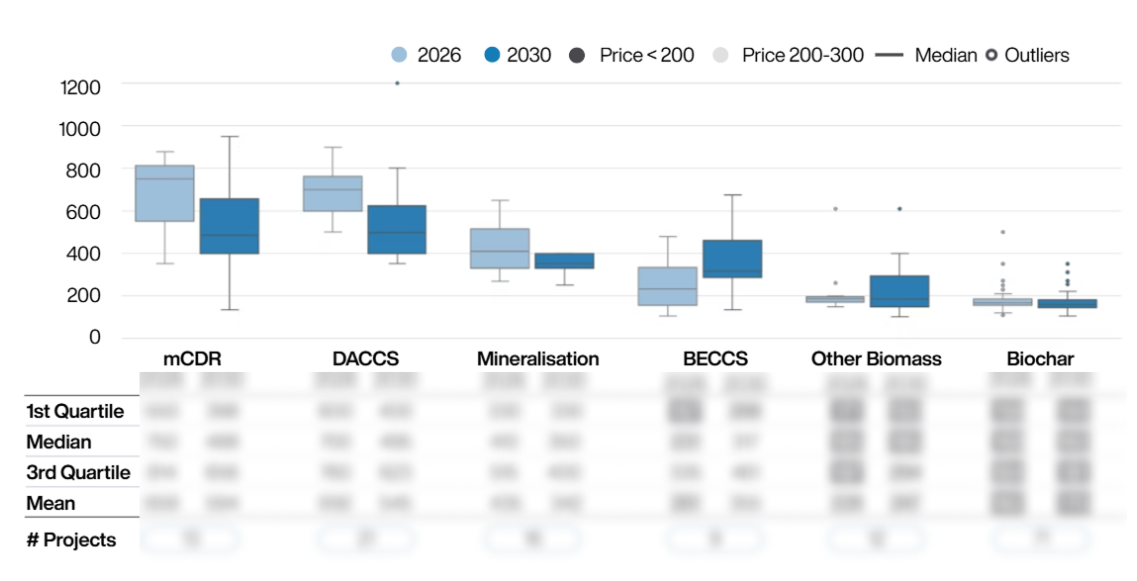

In tandem, price convergence within pathways is accelerating,as suppliers reach operations, achieve verification, and start to build a track record (see Figure 2).

Figure 2: Prices per pathway ($tCO₂) - reach out to the ClimeFi team for the full picture

This evolution is happening in real-time: ClimeFi has already witnessed a visible convergence in prices between the RFPs that we ran in June 2025 and December 2025.

However, it is important to note that this remains an early stage market, with significant room for evolution. While mature pathways like Biochar show signs of convergence, MRV methodologies, quality benchmarks, and regulatory frameworks continue to develop, influencing price strategies adopted by different suppliers.

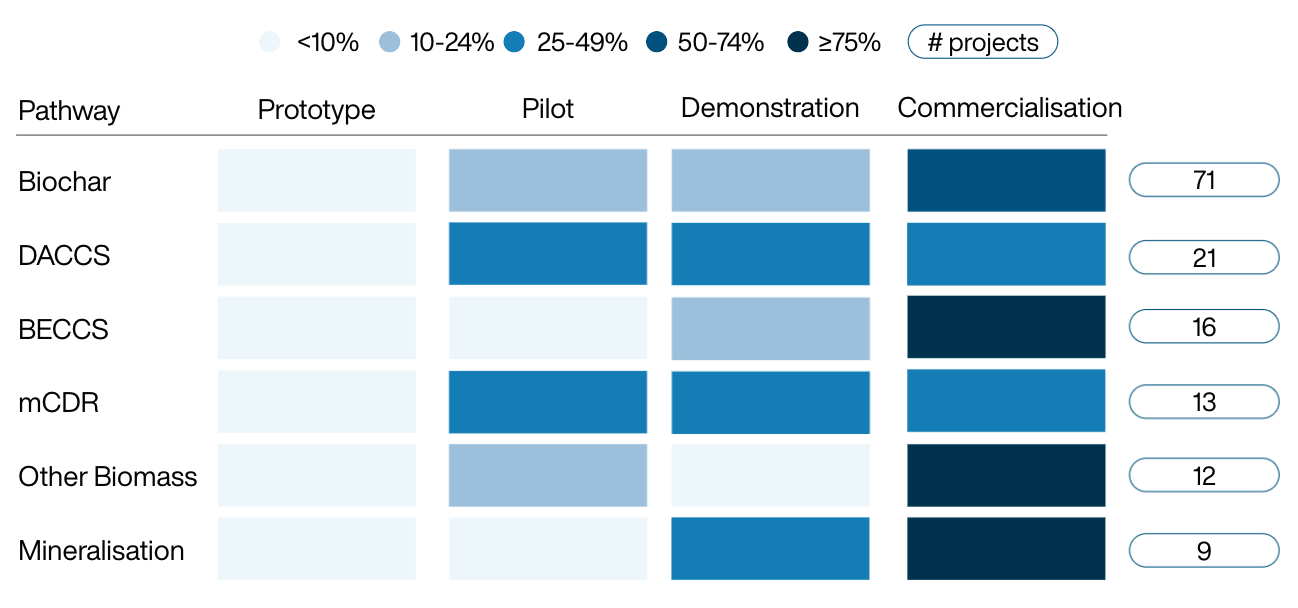

Nonetheless, there are increased signals for growing supplier maturity: 66% of projects are now at the commercialisation stage across all pathways (see Figure 3).

Figure 3: Stage of development (% of pathway’s # of projects)

Biochar's lower barriers to entry have enabled faster commercial deployment, though project quality remains heterogeneous. Meanwhile, DACCS shows the widest distribution of development stages, reflecting a pathway transitioning from demonstration to commercial scale, supported by stronger buyer interest.

No prototype projects were submitted for Marine CDR in the RFP, demonstrating accelerated maturity. While the pathway itself is nascent, early-mover projects have generated operational track records that newer entrants can start building on.

Shifting away from biomass-based CDR

In 2025, credit issuance was dominated by Biochar and BioCCS – the two pathways accounted for 93% of total issuance last year – leaving little room for other pathways to make their mark. 2026 looks set to change that.

While Biochar is still expected to deliver 36% of supply in 2026, there are strong market indications of a shift away from biomass-based CDR and towards a more diversified carbon removal supply, as detailed in Figure 4. This change will largely be driven by large-scale DACCS and BioCCS, as well as smaller ERW and Marine CDR, projects coming online. Industrial facilities such as Stratos (DACCS) and Green Plains (BioCCS) are expected to enter the market and anchor 2026 deliveries.

Not only do we expect greater pathway diversification in 2026, but we also expect total deliveries to increase by 43% year-on-year.

Figure 4: Credits issued in 2025 (tCO₂) vs Credits sold and reserved in 2026 (tCO₂)

Registries up the competition

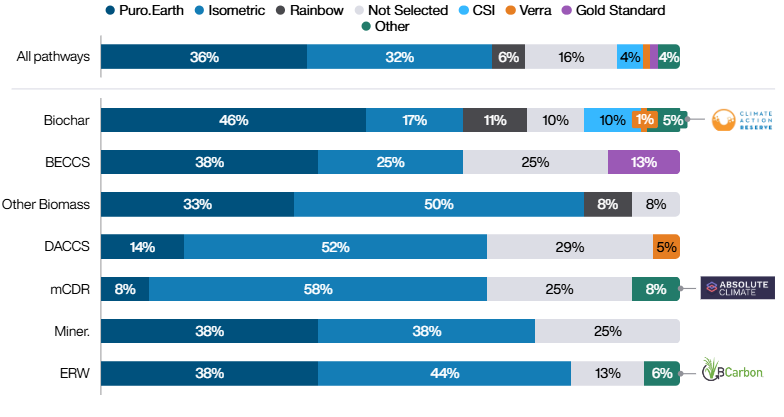

Alongside projects, standards bodies and methodologies are also maturing. As such, registry selection is becoming a much more strategic decision for suppliers, especially as methodologies continue to gain further credibility through various quality certifications such as the ICVCM's CCP labels.

This increased level of competition is already starting to be reflected in the numbers: as many as 16% of projects have not yet selected a registry, pointing to a market that remains fluid as suppliers balance credibility, flexibility, and regulatory uncertainty.

Figure 5: Registry per pathway (as % of # projects)

Puro.earth and Isometric currently lead registry selection with 36% and 32%, respectively, while newer registries such as Rainbow (6%) are also starting to gain exposure within the durable CDR market.

Reach out to the ClimeFi team for deeper insights

If you have any questions about the analysis, or would like to chat to a member of the team, please reach out at procure@climefi.com.

Behind the analysis

ClimeFi ran an RFP for durable carbon dioxide removal (CDR) in December 2025/ January 2026 on behalf of a client, and received submissions from 142 projects, representing 114 suppliers across 39 countries.

Biochar projects accounted for 50% of the submissions, followed by Direct Air Capture with Carbon Storage (DACCS) with 15%, Biomass with Carbon Capture and Storage (BioCCS) with 11%, Marine CDR and Other Biomass CDR* with 9% each, and Mineralisation accounted for 6%. Enhanced Rock Weathering (ERW) was excluded from the RFP, therefore parts of this analysis have incorporated data gathered from our Summer 2025 RFP to ensure fair market assessment. Regionally, North America accounts for the largest share of project submissions (41%), followed by Asia-Pacific (28%), Africa & Middle East (15%), Europe (10%), and South America (6%).

N.B.

- Data for ERW was taken from the RFP run by ClimeFi in the Summer of 2025. All other data is from the RFP run in December 2025.

- Sold and/or reserved capacity was calculated as the difference between total projected capacity and available volumes submitted by suppliers. This figure includes existing customer options and commitments, but may also include capacity held back for other reasons. Suppliers typically withhold volumes due to conservative volume projections, reservations for larger RFPs or long-term contracts, operational buffers (maintenance, quality control), and maintaining pricing flexibility in the market.

- Issuances data includes all issuances registered on Puro.earth, Isometric, and Rainbow in 2025.

- Pricing data is based on indicative base pricing submitted by suppliers in December 2025. These prices are best reflective of a pricing strategy for a <5kt offtake volume.