The problem with sell-side due diligence

Sell-side due diligence is conducted by a party with a direct interest in the supply – either because they own the credits or are otherwise financially exposed to the supplier (e.g., through a commitment to purchase credits in the future). In practice, it's almost the equivalent of asking the supplier to conduct due diligence on itself!

Think about it: if the party preparing the assessment sits on credits on their own balance sheet, a favourable outcome directly reduces their exposure. Disclosing risks does the opposite. That dynamic inevitably shapes what gets scrutiniszed, and what gets conveniently left out.

A lesson from financial markets

None of this is new. In finance, the separation between sell-side and buy-side research has been understood for decades. Sell-side analysts at investment banks cover companies their firm underwrites. Buy-side analysts work solely to inform their own fund's decisions. Regulators eventually had to mandate that separation.

The CDR market does not have the same level of maturity yet, but the underlying problem is the same. To safeguard their reputation and manage exposure, buyers should take lessons from it.

What buy-side due diligence actually looks like

Buy-side due diligence is prepared by a party with no stake in the supply. For corporate buyers, the reputational stakes are high; procurement decisions are increasingly visible to stakeholders, regulators, and the public. Backing the wrong project or overstating the quality of purchased removals can seriously damage credibility. These are the kind of risks a sell-side report has little incentive to surface.

Critically, this isn't just about the initial purchasing decision. Over a multi-year offtake agreement, new risks inevitably emerge: technology setbacks, regulatory changes, counterparty issues, or shifts in project fundamentals. A sell-side provider has little incentive to flag these as they arise. Ongoing, Buy-side monitoring ensures emerging issues are surfaced, not buried.

How to tell the difference

Due diligences are typically not labelled as sell-side or buy-side. When evaluating a diligence provider, the simplest way to assess independence is to understand their exposure to the supply. Does the provider hold credits from the projects it covers, or generate revenue from the suppliers it assesses? Does it have any commercial arrangement, direct or indirect, that ties its financial performance to the success of the supply it is evaluating?

If the answer to either of these is yes, the diligence should be treated accordingly. Useful as a starting point, but not as an independent assessment

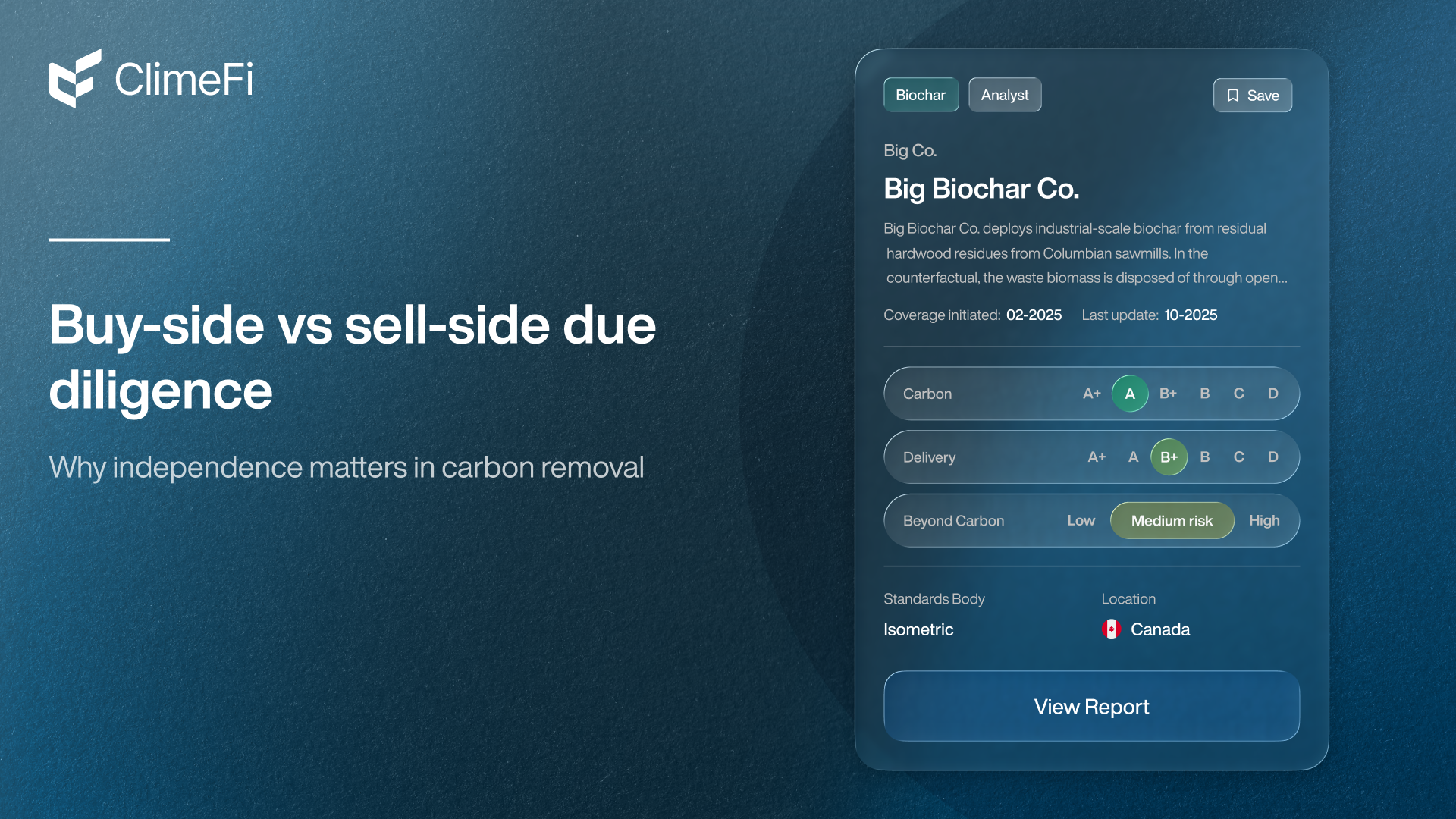

ClimeFi's buy-side diligence library

We recently launched the largest library of buy-side due diligence in the CDR market – 70+ projects with active coverage and ongoing monitoring.

Every assessment is prepared exclusively for buyers, without the conflicts that come with sell-side analysis. We cover key CDR pathways and keep our coverage updated as projects evolve.

If you're evaluating CDR procurement or looking at long-term offtake agreements, request access to our platform to explore our full due diligence coverage.